Private capital in Africa faced numerous challenges in 2023, with factors such as inflation and currency depreciation making business exceptionally tough across the continent. Currencies like the Kenyan shilling and the naira plummeted to historic lows, while a decline in foreign exchange reserves escalated the cost of operations in countries like Egypt.

These conditions significantly impacted private capital activity throughout Africa in 2023, prompting fund managers to adopt a more cautious and prudent approach to their investment strategies.

In April 2024, The African Private Capital Association (AVCA) unveiled its 2023 African Private Capital Activity Report. This report offers valuable insights into dealmaking, fundraising, exits, and the prevailing trends shaping Africa’s private capital landscape. For over two decades, AVCA has been dedicated to facilitating and advocating for private investment across Africa.

- The African market displayed greater resilience than anticipated.

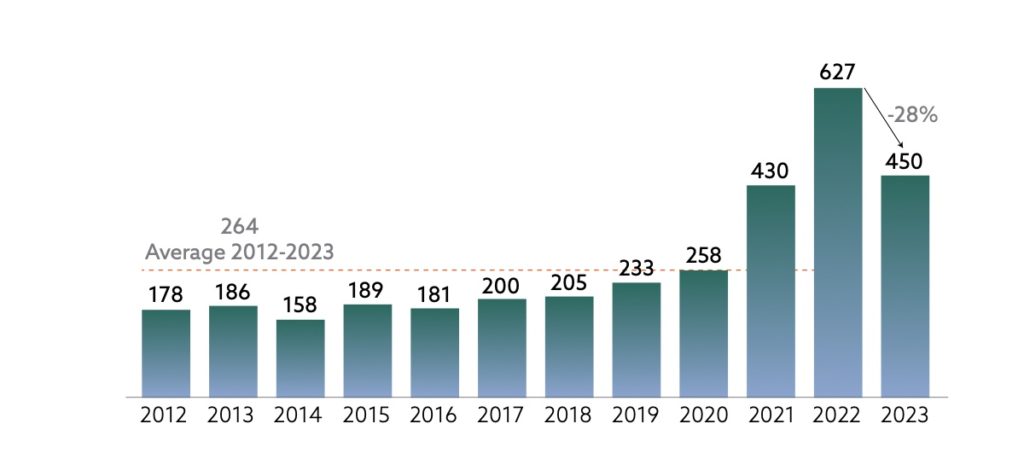

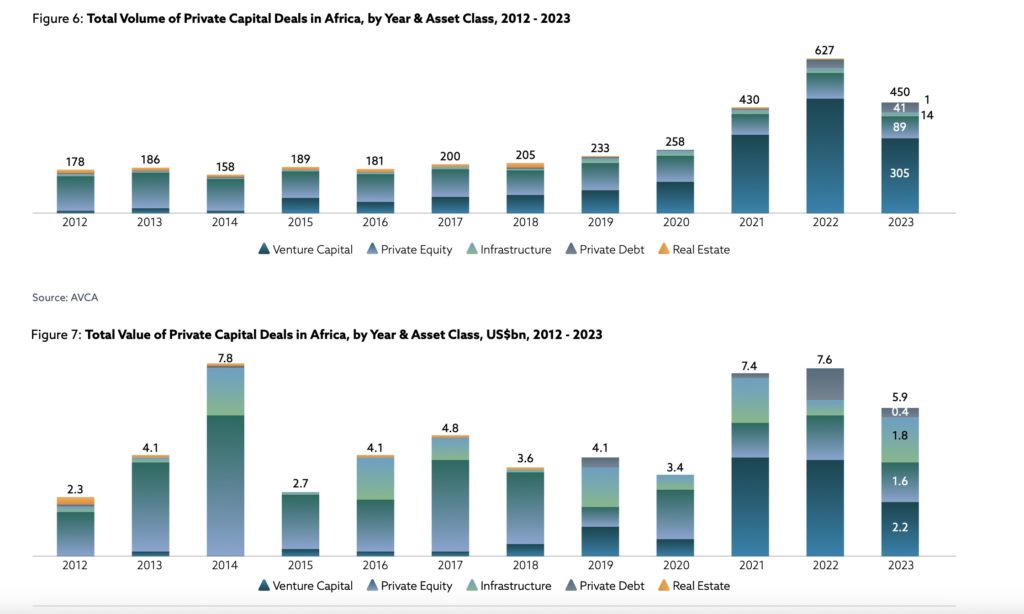

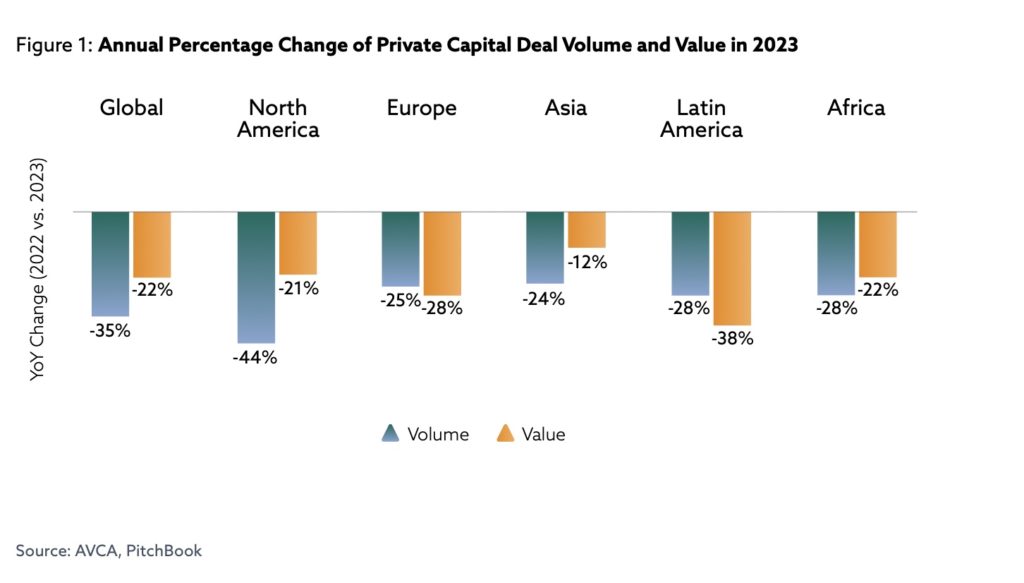

The report highlighted a significant 28% decline in Africa’s total private capital deal volume, resulting in a total of 450 deals. Despite this decrease, Africa showcased unexpected resilience, outperforming other developing regions. The continent still achieved a noteworthy $5.9 billion deal value, marking the second-strongest year on record for deal volume in Africa. This figure surpassed both the decade-long average and recent years’ averages. The robust performance was primarily attributed to two substantial infrastructure investments in South Africa‘s renewable energy sector, each exceeding $250 million.

2. Tech and clean energy received the most attention

Venture capital (VC) maintained its prominent position, capturing 68% of all private capital investment in Africa. This trend underscores investors’ enduring enthusiasm for supporting technology-driven enterprises amid the continent’s swiftly expanding markets, a trend observed since 2015. Following VC, infrastructure also experienced a notable uptick in investment values, tripling to $1.8 billion, primarily propelled by technology energy ventures. The report indicates that investors and industry experts alike are increasingly confident in Africa’s capacity to emerge as a frontrunner in the transition to clean energy in the forthcoming years.

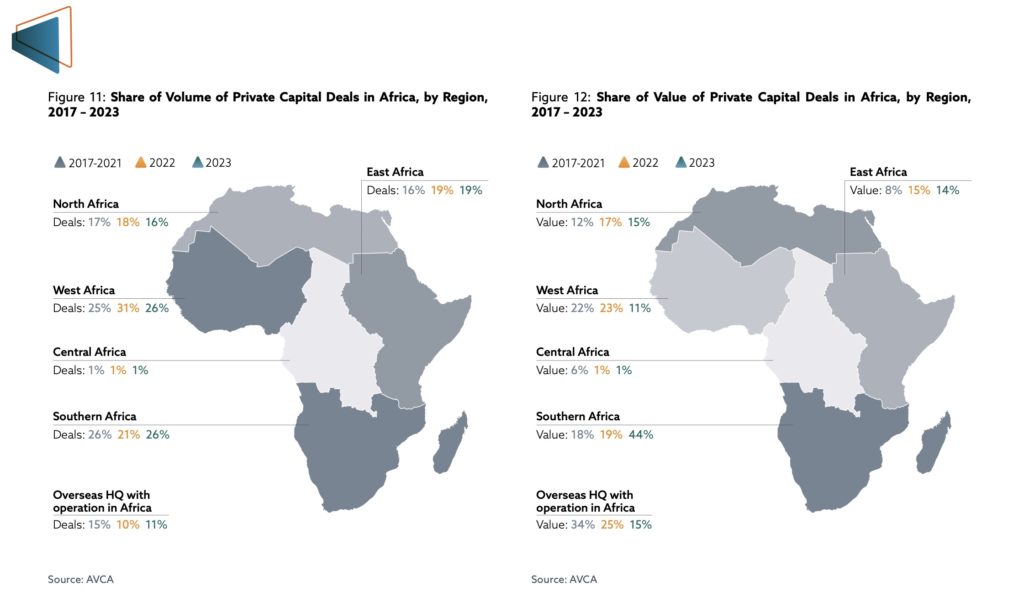

3. Southern Africa is now investors’ favourite investment destination

In 2023, Southern Africa staged a remarkable comeback, reaffirming its status as a leading investment destination. The region secured the highest volume (26%) and value of deals ($2.6 billion), with South Africa leading the charge, buoyed by growth in sectors such as IT, software, logistics, and transportation. Meanwhile, West Africa’s share of the continent’s total private capital deals dwindled to 11%, trailing behind Southern Africa and North Africa. This marked a significant decline from 2022, when West Africa commanded 23% of the total private capital value, while Southern Africa claimed 19%.

4. Investors are still interested in Africa

Although final closed funds, which represent funds ready for investment, experienced a slight decline, there was a notable increase in the average value of capital raised for private debt and venture capital (VC) funds. Despite concerns that the global recession might dampen investor enthusiasm, interim fundraising activity, reflecting capital raised throughout the year, showed some growth, indicating continued interest in the continent. Africa saw a 9% decrease in the total value of fundraising, while Asia experienced a significant 39% decline. In contrast, Europe’s decline was more moderate, standing at just 2%.

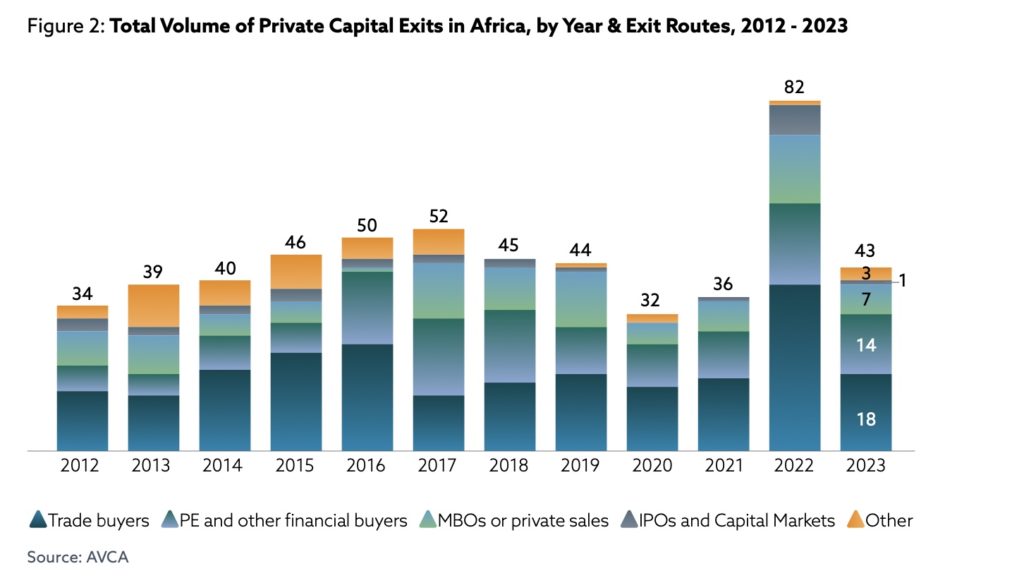

5. Exits are lower than in 2022, but still in line with the average

In 2023, there were 43 exits, marking a notable decrease from the 82 exits observed in 2022. However, this figure still surpasses the 32 and 36 exits recorded in 2020 and 2021, respectively. South Africa maintained its position as the most active exit market, solidifying its status as the prime destination on the continent for mature investments.

Among the exits, there was only one IPO exit, while seven occurred through management sales buyouts (MBOs)/private sales, 18 through trade buyers, and 14 through private equity and financial buyers. Interestingly, for the first time since 2015, there were no exits via the private equity routes within the financial services sector, which was one of the most popular routes in 2022.

Source: TechCabal