In 2022, Charles Archibong had two exits on the table. A role at Yolo Group in Estonia, complete with visa, housing, and a European salary. A contract from Yukawa in Germany, not long after. While friends posted visa approvals and flight tickets, he was in Lagos, staring at an idea that was not fully formed yet, and choosing it anyway.

Two years on, that idea is Myaza, a cross-border payments platform operating across multiple African countries, powered by stablecoin infrastructure, and chasing a target that sounds almost too simple to be hard: make it as easy to send money from Lagos to Nairobi as it is to send a WhatsApp message.

In its first year, Myaza crossed ₦3 billion in transactions, all of it without a single naira spent on paid advertising. In February 2026, the company launched a stablecoin-powered point-of-sale device, letting Lagos businesses accept payment from international customers seamlessly. The next target, Charles says, is doing ₦3 billion in a day.

Technext sat down with him to find out what it actually takes to build cross-border payment infrastructure from Lagos in 2026.

The problem that made Charles Archibong build Myaza

The framing Charles uses most often for what Myaza is solving is a $150 billion gap, that is, the estimated value of cross-border trade in Africa that leaks through friction, high costs, and inaccessibility. He has lived on both sides of that problem. He knows what it feels like to be in Kenya with naira he cannot spend. He has been scammed, blocked, and stranded.

“I saw a $150 billion problem across Africa, and I couldn’t walk away from that. Maybe the bold thing wasn’t leaving. Maybe it was staying.”

But staying, he is quick to say, was not painless. “There are some things I do regret,” he told Technext. “But we move.” Those nights, no money to pay salaries, watching friends post from Berlin and Tallinn while he pushed Flutter code from a Lagos cafe without AC, were real. What kept him was a stubborn conviction that the timing was right and the problem was real.

Stablecoins as infrastructure, not ideology

When most people hear “stablecoin,” they hear a crypto pitch. Charles hears a liquidity fix.

Myaza’s core infrastructure runs on stablecoin rails, a decision he traces directly to an early operational crisis: running out of liquidity while processing high-volume transfers, and having to scramble from bank to bank to cover transactions. The solution was not to raise more capital. It was to change the rails entirely.

“With stablecoins, liquidity is accessible and available at any time you need. That was a simple move that removed the friction we were actually experiencing ourselves. It was not a problem we just had an idea about.”

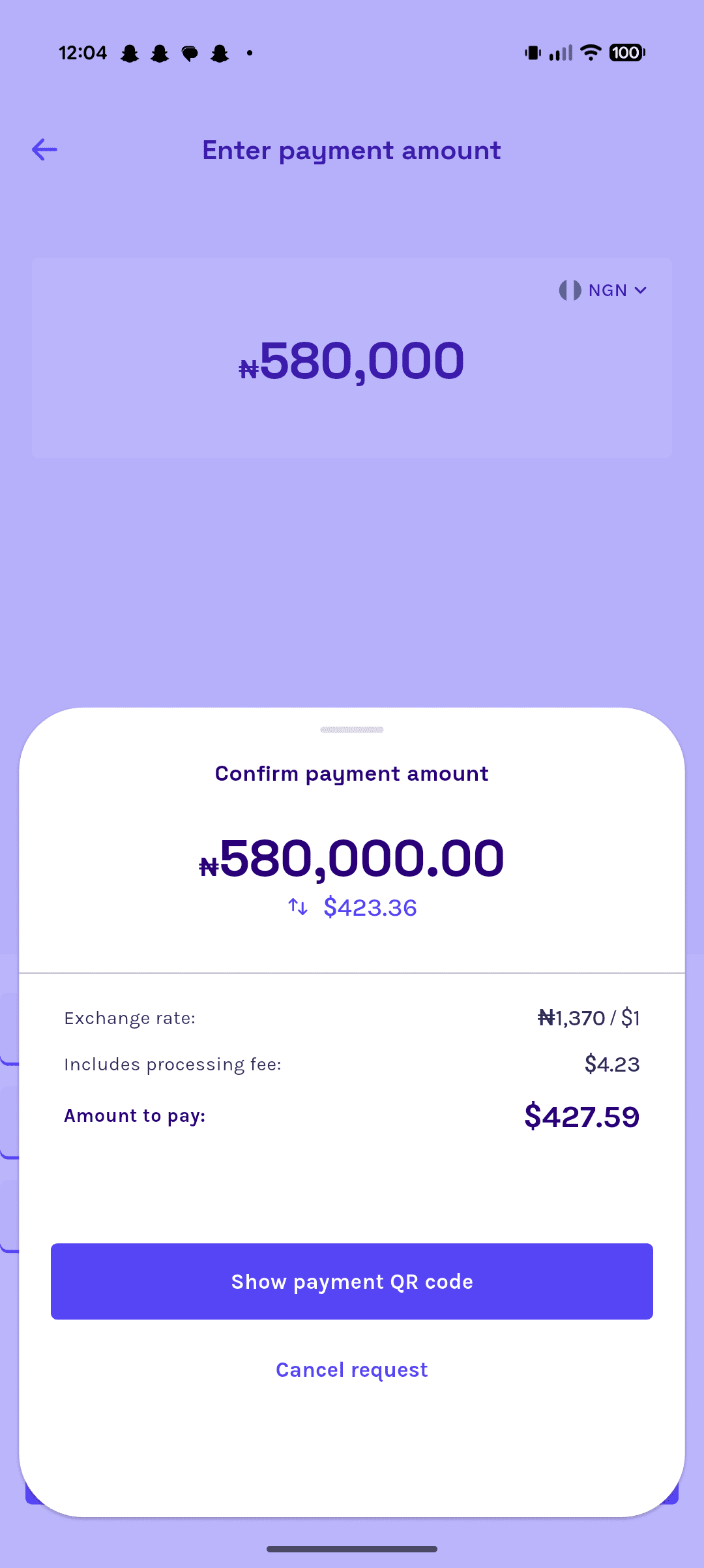

For the average trader using Myaza, say, a Lagos boutique owner trying to receive payment from a customer who flew in from Accra, none of that infrastructure is visible. The platform is built to abstract every layer of blockchain complexity: the swap, the network fees, the liquidity management. What the user sees is a deposit field, a destination, and a recipient. Myaza handles the rest.

“All you need to do is deposit your local currency, select where you want the money to go, provide the recipient details, and we take over the whole swap, trading and liquidity management across blockchain. You don’t have to know anything about blockchain.”

On regulators

The relationship between African payment startups and regulators has historically been tense. Charles remembers when companies in this space would run the other way at the sight of a central bank directive.

He points to the CBN, Bank of Ghana, and the Central Bank of West African States as institutions that are actively engaging with blockchain-based financial products, introducing stablecoin frameworks, studying how blockchain companies operate, and building regulatory playbooks rather than blanket bans. The direction, even if the pace frustrates, gives him confidence.

Read also: Flutterwave, Paystack among 6 companies CBN is supervising as Virtual Asset Providers

One blocker remains. Regulatory fragmentation. Africa has 54 countries and, by his count, just as many different financial rulebooks. The contrast he draws is blunt. The EU’s single currency and unified regulatory framework means a Polish business can pay a German supplier without friction.

The African equivalent, a Pan-African Payment and Settlement System (PAPSS), exists, but Charles is direct about its current state. “That’s still early stages, still testing. At some point, it has had liquidity issues for businesses trying to come on board.” Until PAPSS or something like it matures, companies like Myaza have to navigate each market individually.

The loudest conversation in African fintech in 2026 is B2B infrastructure. Charles agrees with the diagnosis, and positions Myaza squarely inside it, but with a specific focus that narrows the target.

“A lot of people are trading across the border, but only the large corporate companies have access to move money. What Myaza is doing is ensuring that mid-market businesses, up to large-scale corporations, are able to transact seamlessly, without needing expensive bank requirements before they can sell to someone in a different country.”

The gap he is describing is real. Large multinationals have treasury teams and correspondent banking relationships. Individual consumers have remittance apps. The middle layer, an Abuja-based manufacturer paying a supplier in Dakar, a Nairobi logistics company settling invoices with a partner in Lagos, has historically been underserved by both.

Myaza’s B2B infrastructure play targets exactly that segment: receiving payments, moving money, and settling invoices across the continent without the friction that currently makes cross-border trade feel like an obstacle course.

The growth playbook and why it will not scale forever

₦3 billion in year one, with zero paid advertising. The story is striking enough that it is worth pressing on.

The actual mechanism, Charles explains, was simpler than the result suggests: social media content that educated people about intra-African payments, travel, and cross-border business, with Myaza inserted into the conversation at the right moment, sometimes directly, sometimes through comments on other people’s posts.

“From one customer, word of mouth spread,” he says. “It was quite shocking that the little comments, the little videos we were creating, were actually making an impact in our numbers.”

He is clear-eyed that the model has a ceiling. “That model cannot give us the volume we are looking forward to today.”

When Technext pushed for specifics on what replaces it, he declined, deliberately. The distribution strategy, he says, is a trade secret. When they find a channel that works, they exploit it fully before moving to the next one. Sharing it publicly hands the playbook to competitors in a market where, as he points out, the technical barriers to building a cross-border payment product are now relatively low.

“It’s quite easy for anyone to build a cross-border payment solution with how accessible blockchain is today. But distribution is where people always get it wrong. When we discover it, we keep it secret. We exploit it till we are done with that distribution channel. Then we look for another one.”

The Stablecoin POS

In February 2026, Myaza launched a stablecoin-powered point-of-sale device aimed at Lagos businesses with significant international customer traffic – boutiques, fashion stores, wine shops, clubs. The device accepts international payments, and either converts the proceeds to naira for instant payout to the merchant’s local account, or routes the funds to a dollar account if the merchant prefers.

The pitch to merchants, Charles says, writes itself. A tourist or diaspora visitor lands in Lagos and wants to buy something at a boutique on Victoria Island. Their international card may or may not work. Even if it does, the merchant has to figure out what to do with the foreign currency. The stablecoin POS removes both problems at once.

“The money lands, the POS changes it to naira and pays it out to your business account. Or if you don’t want that, you can push it to your US bank account. You don’t have to worry about when I receive this USD, what do I do with it? How do I move it to my Nigerian bank so I can pay my suppliers?”

The product is in active pilot across select Lagos merchants, including gadget stores, fashion retailers, and hospitality venues, among them. Charles says the onboarding process is straightforward: a business assessment, verification of international customer activity, and KYB checks. The device ships once the merchant clears compliance.

Two years in

The headline question Charles gets most often is some version of: was staying worth it? He does not express certainty about the answer. What he is certain about is the direction of the industry.

Stablecoins, he argues, are the single biggest unlock African financial infrastructure has seen in years, not just for cross-border payments, but for cards, settlement, and merchant acceptance.

The CBN’s evolving posture on virtual assets, the BCEAO’s new instant payment rail, and the growing sophistication of mid-market B2B payment demand are all moving in the same direction.

The goal Myaza is now chasing, processing in a single day what it took a year to do in 2024, depends on all of that infrastructure maturing at the same time. Charles is betting that it will, and that the companies that built real rails while the market was still early will be the ones who define what African cross-border trade looks like when it finally breaks through.

“Real wealth is in building something that serves your people. That’s what I’m trying to do. That’s what Myaza is about.”