For years, the narrative surrounding cryptocurrency in Nigeria has been dominated by a singular transactional loop: buy, hold, and off-ramp into local fiat. Amidst soaring inflation and currency volatility, digital assets have largely been treated as speculative vehicles or temporary safe havens rather than functional money.

However, a fundamental paradigm shift is currently unfolding across the African Web3 ecosystem. Local, innovative Web3 platforms are moving beyond mere liquidation to build integrated, everyday financial rails powered by the blockchain.

At the forefront of this evolution is Busha, one of the continent’s pioneering crypto-fiat platforms.

In an exclusive with Technext, Oluwadara Openiyi, product manager, explained how the company is expanding crypto utility across sub-Saharan Africa, beyond basic exchange services, to forge an integrated, real-world financial ecosystem.

From crypto-backed liquidity lines to seamless B2B institutional API integrations, Busha is engineering a future where digital assets and traditional rails do not just coexist but converge.

To understand Busha’s product architecture, one must first dismantle the narrow perception of what crypto utility actually means.

“Crypto is digital assets, your Bitcoin, your USDT, stablecoins, or altcoins,” Openiyi explains. “And utility is just practical use. When we talk about crypto utility, we talk about spending your crypto, using your crypto in practical, real-world experiences, and unlocking that real-world value.”

The company has embedded this practical philosophy into its rebranded ‘Busha Spend’ feature, now known as Pay Bill. The platform enables users to seamlessly incorporate digital assets into their daily routines.

Customers can purchase mobile data, buy airtime, and pay for electricity or television subscriptions directly from their crypto balances. They can even spend their digital funds at local supermarkets, spas, and ice cream parlours.

Crucially, this feat is achieved without forcing local merchants or utility giants to navigate the complexities of Web3. At the user interface level, balances leave a customer’s crypto wallet, but Busha seamlessly settles the transaction with telecommunications and utility partners in local fiat behind the scenes.

Unsurprisingly, stablecoins are driving these daily transactions. Because assets like USDT retain near-perfect parity with the US dollar, users vastly prefer them for daily spending to preserve their purchasing power.

Yield and crypto-backed loans

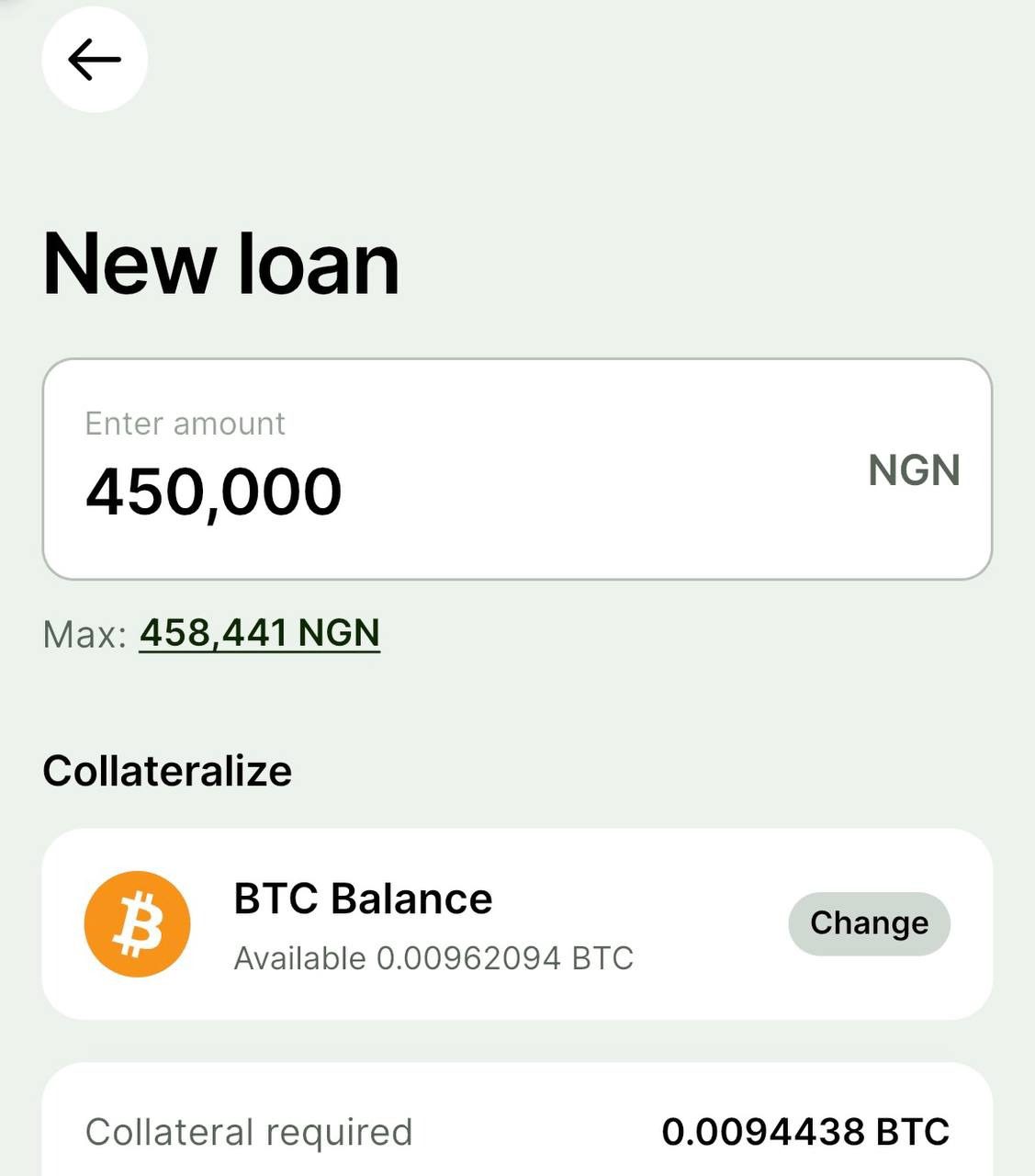

A recurring structural challenge for local crypto holders is the pressure to liquidate digital assets during sudden cash crunches. Busha addresses this directly through its crypto-backed loans.

This feature allows users to collateralise their Bitcoins or USDTs to access immediate Naira liquidity without selling their holdings. The loans attract a modest 2% interest rate. Once the borrower repays the fiat value, Busha safely releases the underlying digital assets back to the user.

Interestingly, the primary driver for these loans is not always personal emergencies. Market behaviour reveals a much more strategic, crypto-native approach.

“The trend that we’ve seen is customers taking these loans for the short term,” Openiyi notes. ” Most of the time, they take out loans to buy a particular asset because they can see that the asset is going up, and they want to add to it.”

Managing the risk of volatile loan-to-value (LTV) ratios in a market as unpredictable as Nigeria requires strict operational parameters. Busha enforces a robust risk management protocol: the platform caps loans strictly at the immediate fiat valuation of the collateralised asset, ensuring complete downside protection for both the borrower and the platform if sudden market liquidation triggers occur.

Beyond credit, Busha Savings (formerly Busha Yield and Busha Earn), which previously offered high-yield stablecoin products, has strategically expanded to cover traditional financial products, currently offering up to 20% per annum on NGN savings and a risk-mitigated 7.5% per annum on USD savings.

Building advanced financial tools is only half the battle. The other half is ensuring that everyday users are not intimidated by them.

Global crypto exchanges are notoriously data-heavy, often greeting users with complex candlestick charts and dense technical jargon. Busha has explicitly championed a clean, minimalist user interface (UI) to counter this market friction.

When constructing intricate features like automated recurring buys or loan dashboards, the platform prioritises absolute simplicity. Around six months ago, Busha launched a completely redesigned app interface. The core philosophy was straightforward: maintain a clean UI with easy-to-read copy.

“One of our core values when building is to include simplicity in the app,” Openiyi explains. “We are conscious not to spam our users, but we are also conscious to make sure they are informed.”

The platform ensures that users understand the implications behind every action, breaking down complex digital finance concepts into terms as simple as “ABC123”. It is a deliberate strategy to demystify the blockchain for the broader African retail market.

Also read: Here are 8 startups enabling Nigerians to spend crypto easily

The B2B institutional convergence

Beyond its consumer-facing utilities, Busha has built a dedicated B2B infrastructure arm, Busha Business, designed for companies, fintechs, and developers that need licensed financial rails to operate across borders.

The platform gives businesses access to cross-border payments, stablecoin treasury management to protect reserves from local currency depreciation, and USD and naira savings products that earn daily interest on idle capital. For merchants, Busha Pay enables businesses to accept stablecoin payments from customers anywhere in the world and receive settlement in USD.

Underpinning all of this is an API stack built on Nigeria’s first SEC-licensed digital asset infrastructure, giving fintechs and developers the ability to embed payments, wallets, stablecoin settlement, FX conversion, and KYC/KYB into their own products without building from scratch

This reliable infrastructure is attracting significant traditional players to the Web3 ecosystem.

“We have clients in the aviation industry and oil and gas; we have importers and exporters and fintechs that use our APIs,” says Openiyi. “All of these industries take advantage of our stablecoin offerings and our APIs. There is massive adoption.”

Historically, the relationship between Web3 firms and traditional financial institutions in Nigeria has been fraught with friction. However, as a formally licensed digital asset exchange, Busha has built its product pipeline around absolute regulatory alignment.

The platform’s upcoming virtual and physical USD debit cards, designed to allow local professionals to spend globally powered by stablecoins, are built entirely in lockstep with central regulations.

“We are a compliance-by-design-led company,” Openiyi emphasises. “Even from conception, we ensure that compliance is involved and our regulators are involved before we even build. What the licence did for us was more for our customers; it created more trust and security.”

This institutional credibility is fostering a unique structural convergence. Rather than a zero-sum game between Web3 and legacy banking, both ecosystems are moving toward mutual integration. Traditional finance realises it needs the speed and efficiency of cryptographic rails, while Web3 platforms require the foundational infrastructure of regulated fiat banking.

If the product infrastructure is ready and the regulatory framework is solidifying, what stands between Nigeria and a truly circular crypto economy? For Busha’s leadership, the final barrier isn’t technical; it’s educational.

Achieving widespread grassroots utility by 2030 will require moving past high-level industry echo chambers. It demands inclusive, hyper-localised marketing that speaks to the everyday trader, market woman, and corporate executive alike.

With the emergence of institutional adoption and the expansion of regulated frameworks, the foundation for sub-Saharan Africa’s new financial architecture has shifted from an abstract concept to a real-world reality.